In a standard bank account, any interest we earn is automatically added to our balance, and we earn interest on that interest. This reinvestment of interest is called compounding. We will develop the mathematical formula for compound interest and then show the equivalent spreadsheet function.

Subsection 3.4.1 Introduction to Compound Interest

Suppose that we deposit $1000 in a bank account offering 3% interest, compounded monthly. How will our money grow?

The 3% interest is an annual percentage rate (APR) – the total interest to be paid during the year. Since interest is being paid monthly, each month, we will earn \(\frac{0.03}{12}=0.0025\) per month.

In the first month,

\begin{align*}

P\amp= \$1000\\

r\amp=0.0025\\

I\amp= \$1000 (0.0025)= \$2.50\\

A\amp= \$1000 + \$2.50 = \$1002.50

\end{align*}

In the first month, we will earn $2.50 in interest, raising our account balance to $1002.50.

In the second month,

\begin{align*}

P\amp=\$1002.50\\

I\amp=\$1002.50(0.0025)=\$2.51 \text{ (rounded)}\\

A\amp=\$1002.50+\$2.51=\$1005.01

\end{align*}

Notice that in the second month we earned more interest than we did in the first month. This is because we earned interest not only on the original $1000 we deposited, but we also earned interest on the $2.50 of interest we earned the first month. This is the key advantage that compounding gives us.

Calculating out a few more months in a table or a spreadsheet we have:

| 1 |

1000.00 |

2.50 |

1002.50 |

| 2 |

1002.50 |

2.51 |

1005.01 |

| 3 |

1005.01 |

2.51 |

1007.52 |

| 4 |

1007.52 |

2.52 |

1010.04 |

| 5 |

1010.04 |

2.53 |

1012.57 |

| 6 |

1012.57 |

2.53 |

1015.10 |

| 7 |

1015.10 |

2.54 |

1017.64 |

| 8 |

1017.64 |

2.54 |

1020.18 |

| 9 |

1020.18 |

2.55 |

1022.73 |

| 10 |

1022.73 |

2.56 |

1025.29 |

| 11 |

1025.29 |

2.56 |

1027.85 |

| 12 |

1027.85 |

2.56 |

1030.42 |

To find an equation to calculate future balances more efficiently, we will go through a few months to see the pattern:

Initial Amount: \(P=\$1000\)

\(1^{\text{st}} \text{ Month } A=1.0025(\$1000)\)

\(2^{\text{nd}} \text{ Month } A=1.0025(1.0025(\$1000))=1.0025^{2}(\$1000)\)

\(3^{\text{rd}} \text{ Month } A=1.0025(1.0025^{2}(\$1000))=1.0025^{3}(\$1000)\)

\(4^{\text{th}} \text{ Month } A=1.0025(1.0025^{3}(\$1000))=1.0025^{4}(\$1000)\)

Observing a pattern, we could conclude

\(m^{\text{th}} \text{ Month } A=1.0025^{m}(\$1000)\)

If we wanted to calculate the balance after 15 years, we observe that 15 years is equal to \(15\cdot12=180\) months. This results in

\begin{equation*}

1.0025^{180}(\$1000)\approx\$1567.43

\end{equation*}

Notice that the $1000 in the equation was P, the starting amount. We found 1.0025 by adding one to the interest rate divided by 12, since we were compounding 12 times per year. This approach is generalized to the formula that follows.

Compound Interest.

\begin{equation*}

A=P\left(1+\frac{r}{n}\right)^{nt} \text{ or } P=A \left(1+\frac{r}{n}\right)^{-nt}

\end{equation*}

where

- A

is the future value balance in the account after \(t\) years

- P

is the principal or present value

- r

is the annual interest rate in decimal form

- n

is the number of compounding periods in one year

- t

is the number of years

Note that the exponent \(nt\) is equal to the total number of periods.

If the compounding is done annually (once a year), \(n = 1\text{.}\)

If the compounding is done quarterly, \(n = 4\text{.}\)

If the compounding is done monthly, \(n = 12\text{.}\)

If the compounding is done weekly, \(n = 52\text{.}\)

If the compounding is done daily, \(n = 365\text{.}\)

The most important thing to remember about using this formula is that it assumes that we put money in the account once and let it sit there earning interest.

Subsubsection 3.4.1.1 Comparing Simple and Compound Interest

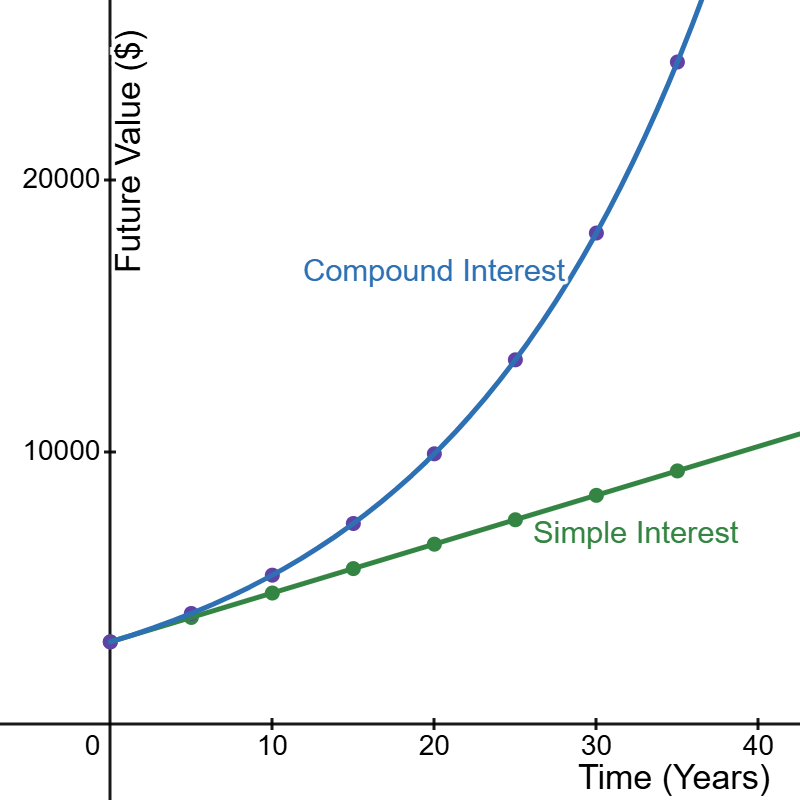

Let us compare the amount of money earned from compounding in the previous example against the amount you would earn from simple interest. From the table and graph below we can see that over a long period of time, compounding makes a large difference in the account balance.

| 0 |

$3,000 |

$3,000 |

| 5 |

$3,900 |

$4,046.55 |

| 10 |

$4,800 |

$5,458.19 |

| 15 |

$5,700 |

$7,362.28 |

| 20 |

$6,600 |

$9,930.61 |

| 25 |

$7,500 |

$13,394.91 |

| 30 |

$8,400 |

$18,067.73 |

| 35 |

$9,300 |

$24,370.65 |

You may have observed that simple interest has linear growth while compound interest has exponential growth. This is because with simple interest, the amount of interest earned each year is the same. While simple interest is based on a percentage, that percentage is calculated only once on the original amount and the amount of increase each year remains constant. With compound interest, the percentage of interest is applied each period, so the amount of interest earned each year increases as the account balance increases.

Subsection 3.4.2 Applications of Compound Interest

Example 3.4.2. Finding a Future Value.

A certificate of deposit (CD) is a savings instrument that many banks offer. It usually gives a higher interest rate than regular savings accounts, but you cannot access your investment for a specified length of time. Suppose you deposit $3000 in a CD paying 6% APR, compounded monthly. How much will you have in the account after 20 years?

Solution.

\(P = \$3\,000\text{,}\) the initial deposit

\(r = 0.06\text{,}\) 6% annual rate

\(n = 12\text{,}\) 12 months in 1 year

\(t = 20\text{,}\) since we’re looking for how much we’ll have after 20 years

\begin{equation*}

A=P\left(1+\frac{r}{n}\right)^{nt}=3000\left(1+\frac{0.06}{12}\right)^{12\cdot 20}\approx$9930.61

\end{equation*}

Therefore, we will end up with approximately $9,930.61 after 20 years.

In the example above, an initial deposit of $3,000 grew to $9,930.61 in 20 years. The difference between these two amounts, $6,930.61, is the amount of interest earned on the initial deposit. This is more than double the original deposit!

Example 3.4.3.

If you deposit $20,000 in a CD paying 4% APR, compounded quarterly, how much interest will you earn in 5 years?

Solution.

\(P = \$20\,000\text{,}\) the initial deposit

\(r = 0.04\text{,}\) 4% annual rate

\(n = 4\text{,}\) 4 quarters in 1 year

\(t = 5\text{,}\) since we’re looking for how much we’ll have after 5 years

\begin{equation*}

A=P\left(1+\frac{r}{n}\right)^{nt}=20000\left(1+\frac{0.04}{4}\right)^{4\cdot 5}\approx\$24{,}403.80

\end{equation*}

The amount of interest earned is the final balance minus the initial deposit, which is the difference between the starting value of $20,000 and the final value of $24,403.80. Therefore, the interest earned is $4,403.80.

Example 3.4.4.

What is the future value of a $5000 deposit in an account that pays 3% APR compounded monthly after 5 months?

Solution.

Using the compound interest formula, we have

\begin{align*}

A\amp= P\left(1+\frac{r}{n}\right)^{nt}\\

A\amp=5000\left(1+\frac{0.03}{12}\right)^{12\cdot \frac{5}{12}}\\

A\amp=5000\left(1+\frac{0.03}{12}\right)^{5} \\

A\amp\approx\$5062.80

\end{align*}

The future value of the $5000 deposit after 5 months is approximately $5062.80.

Notice that the time was given in months, so we converted it to years to obtain \(t=\frac{5}{12}\text{;}\) then the exponent became \(12\cdot\frac{5}{12}=5\text{.}\) However, we could have also remembered that the exponent is always equal to the number of compounding periods and directly entered the exponent as 5 without converting the time to years first.

When we know the amount of money we want to have in the future, we can use the formula that is solved for P.

Example 3.4.5. Finding a Present Value.

You know that you will need $40,000 for your child’s education in 18 years. If your account earns 4% APR compounded quarterly, how much would you need to deposit now to reach your goal?

Solution.

We will use the form of the compound interest formula in which P is isolated.

\(r = 0.04\text{,}\) 4% APR

\(n = 4\text{,}\) 4 quarters in 1 year

\(t = 18\text{,}\) since we know the balance in 18 years

\(A = \$40{,}000\text{,}\) the amount we have in 18 years

\begin{equation*}

P=A\left(1+\frac{r}{n}\right)^{-nt}=40000\left(1+\frac{0.04}{4}\right)^{-4\cdot 18}\approx\$19{,}539.84

\end{equation*}

You would need to deposit $19,539.84 now to have $40,000 in 18 years.

In the examples below, we will need to set up and solve algebraic equations to solve for the time or rate.

Example 3.4.6. Solving for the Time.

You want to have $10,000 in an account that pays 5% APR compounded annually. If you deposit $5000 now, how long will it take to reach your goal?

Solution.

We do not have a form of the compound interest formula in which t is isolated, so we will need to use logarithms to solve for t.

\(P = \$5{,}000\text{,}\) the initial deposit

\(A = \$10{,}000\text{,}\) the desired balance

\(r = 0.05\text{,}\) the annual interest rate

\(n = 1\text{,}\) since it’s compounded annually

\begin{align*}

A \amp= P\left(1+\frac{r}{n}\right)^{nt}\\

10000\amp=5000\left(1+\frac{0.05}{1}\right)^{1\cdot t}\\

10000\amp=5000(1.05)^{t}\\

2\amp=(1.05)^{t}\\

\log(2) \amp= \log\left((1.05)^{t}\right) \\

\log(2)\amp=t\cdot \log(1.05)\\

t\amp=\frac{\log(2)}{\log(1.05)}\approx14.21

\end{align*}

It will take approximately 14.21 years to reach your goal of $10,000.

In the previous example, we were able to simplify the equation to \(2=(1.05)^{t}\) before taking logarithms. If the base of the exponent cannot be simplified in this way, we can still use logarithms to solve for the unknown variable; we will just leave the base in the form \(1+\frac{r}{n}\) as seen in the next example.

Example 3.4.7.

You want to have $10,000 in an account that pays 5% APR compounded monthly. If you deposit $3,000 now, how long will it take to reach your goal?

Solution.

Using the compound interest formula, we have

\begin{align*}

A \amp= P\left(1+\frac{r}{n}\right)^{nt} \\

10000\amp=3000\left(1+\frac{0.05}{12}\right)^{12t}\\

\frac{10}{3}\amp=\left(1+\frac{0.05}{12}\right)^{12t}\\

\log \left(\frac{10}{3}\right) \amp= \log\left(\left(1+\frac{0.05}{12}\right)^{12t}\right) \\

\log\left(\frac{10}{3}\right)\amp=12t \cdot\log\left(1+\frac{0.05}{12}\right)\\

t\amp=\frac{\log\left(\frac{10}{3}\right)}{12\log\left(1+\frac{0.05}{12}\right)}\approx24.13

\end{align*}

It will take approximately 24.13 years to reach your goal of $10,000.

In the example above, we used logarithms to solve for the equation because the variable was in the exponent. When solving for the interest rate, the variable is in the base of the exponent, so we will use radicals instead of logarithms in the solution.

Example 3.4.8. Solving for the Interest Rate.

You want to have $15,000 in an account that pays interest compounded annually. If you deposit $3,000 now and want to reach your goal in 15 years, what interest rate do you need? Round to the nearest hundredth of a percent.

Solution.

Using the compound interest formula, we have

\begin{align*}

A \amp= P\left(1+\frac{r}{n}\right)^{nt}\\

15000 \amp= 3000\left(1+\frac{r}{1}\right)^{1 \cdot 15}\\

5 \amp= (1+r)^{15}\\

\sqrt[15]{5} \amp= 1+r\\

r \amp= \sqrt[15]{5} - 1\\

r \amp\approx 0.1133 \text{ or } 11.33\%

\end{align*}

You would need an interest rate of approximately 11.33% to reach your goal.

Note: If your calculator does not have a key for the nth root, you can use the fact that the 15th root of 5 is the same as 5 raised to the power of \(\frac{1}{15}\text{.}\) This is entered as \(5\text{^}{\left(1\div 15\right)}\text{.}\)

In the previous example, the compounding was done annually and the ending value was a multiple of the starting value, so we were able to simplify the equation to \(5=(1+r)^{15}\) before taking the 15th root. If the compounding is done more frequently or the ending value is not a nice round number, we can still use radicals to solve for the unknown variable; we will just leave the base in the form \(1+\frac{r}{n}\) as seen in the next example.

Example 3.4.9.

What interest rate is required for an initial investment of $3,000 to reach a value of $11,000 in 15 years if interest is compounded monthly? Round to the nearest hundredth of a percent.

Solution.

Using the compound interest formula, we have

\begin{align*}

A \amp= P\left(1+\frac{r}{n}\right)^{nt} \\

11000 \amp= 3000\left(1+\frac{r}{12}\right)^{12 \cdot 15} \\

\frac{11}{3} \amp= \left(1+\frac{r}{12}\right)^{180} \\

\sqrt[180]{\frac{11}{3}} \amp= 1+\frac{r}{12} \\

\frac{r}{12} \amp= \sqrt[180]{\frac{11}{3}} - 1 \\

r \amp= 12\left(\sqrt[180]{\frac{11}{3}} - 1\right) \\

r \amp\approx 0.0869 \text{ or } 8.69\%

\end{align*}

You would need an interest rate of approximately 8.69% to reach your goal.

Subsection 3.4.4 Annual Percentage Yield (APY)

If you are shopping around for different investments, you might need to compare different rates that have different compounding periods. If the rate and period are different, it’s hard to know which account will give the better result. For example, is it better to invest in an account earning 3% interest with daily compounding or 3.02% interest with semiannual compounding?

To compare, let’s imagine that $1,000 is invested in each account at the end of one year. The account with 3% interest with daily compounding would give us

\begin{equation*}

A=1\,000\left(1+\frac{0.03}{365}\right)^{365\cdot 1}\approx\$1\,030.45.

\end{equation*}

The account with 3.02% interest with semiannual compounding would give us

\begin{equation*}

A=1\,000\left(1+\frac{0.0302}{2}\right)^{2\cdot 1}\approx\$1\,030.43.

\end{equation*}

We can find the interest earned as a percentage of the initial investment for each account. For the 3% interest with daily compounding, we have \(\frac{30.45}{1000}=0.03045\text{ or }3.045\%\text{.}\) For the 3.02% interest with semiannual compounding, we have \(\frac{30.43}{1000}=0.03043\text{ or }3.043\%\text{.}\) The account with 3% interest with daily compounding gives a slightly higher return in this case.

The percentage that we calculated for each account is called the annual percentage yield (APY), also called the effective annual rate (EAR). The APY is the actual interest rate that you will earn on an account after compounding. It is a tool for comparing accounts with different rates and compounding periods.

We could have calculated the APY for each account without calculating the future value first or even knowing the principal. In the example above, we first calculated the future value after one year using the compound interest formuula with \(t=1\text{.}\) Then we subtracted the principal \(P\text{.}\) Finally, we divided that result by the principal. Putting this into a formula, we get:

\begin{equation*}

APY = \frac{P\left(1+\frac{r}{n}\right)^{nt}-P}{P}

\end{equation*}

which simplifies to

\begin{equation*}

APY = \left(1+\frac{r}{n}\right)^{n}-1

\end{equation*}

Example 3.4.11.

Find the APY for an account that pays 4.5% with monthly compounding. Round to the nearest hundredth of a percent.

Solution.

Using the formula for APY, we have

\begin{equation*}

APY=\left(1+\frac{0.045}{12}\right)^{12}\approx 0.04594\text{ or }4.59\%

\end{equation*}

Example 3.4.12.

Which is a better deal: 10.5% with daily compounding or 10.6% with quarterly compounding?

Solution.

We calculate the APY for each account. For the 10.5% APR compounded daily, we have

\begin{equation*}

APY=\left(1+\frac{0.105}{365}\right)^{365}\approx 0.11069\text{ or }11.07\%

\end{equation*}

and for the 10.6% APR compounded quarterly, we have

\begin{equation*}

APY=\left(1+\frac{0.106}{4}\right)^{4}\approx 0.11029\text{ or }11.03\%

\end{equation*}

The account with 10.5% APR compounded daily has a higher APY, so it is the better deal.

Example 3.4.13.

What nominal interest rate with monthly compounding would give the same APY as 4.6% with quarterly compounding?

Solution.

To solve this, we set the APY for the monthly compounding in terms of \(r\) equal to the APY for the quarterly compounding with \(r=4.6\%\) and solve for \(r\text{.}\)

\begin{align*}

\left(1+\frac{r}{12}\right)^{12}-1 \amp =\left(1+\frac{0.046}{4}\right)^{4}-1 \\

\left(1+\frac{r}{12}\right)^{12} \amp =\left(1+\frac{0.046}{4}\right)^{4} \\

\sqrt[12]{\left(1+\frac{r}{12}\right)^{12}} \amp =\sqrt[12]{\left(1+\frac{0.046}{4}\right)^{4}} \\

1+\frac{r}{12} \amp =\sqrt[12]{\left(1+\frac{0.046}{4}\right)^{4}} \\

\frac{r}{12} \amp =\sqrt[12]{\left(1+\frac{0.046}{4}\right)^{4}} - 1 \\

r \amp = 12\left(\sqrt[12]{\left(1+\frac{0.046}{4}\right)^{4}} - 1\right) \\

r \amp\approx 0.0459 \text{ or } 4.59\%

\end{align*}

Therefore, a nominal interest rate of approximately 4.59% with monthly compounding would give the same APY as 4.6% with quarterly compounding.

Subsection 3.4.5 Using Spreadsheets for Compound Interest Applications

Spreadsheets have several built-in functions that apply the formulas in this section. The spreadsheet functions to make calculations more quickly and efficiently, but they should not be used as a replacement for understanding the underlying mathematics or learning how to use the formulas. The formulas pertaining to compound interest are listed below. We will add to this list of formulas in the next section.

Annual Percentage Yield (APY).

=EFFECT(nominal rate, npery)

nominal rate is the stated interest rate (APR) and is entered as a decimal.

npery is the number of compounding periods per year.

Example 3.4.14.

Find the APY for an account that pays 4.5% with monthly compounding. Round to the nearest hundredth of a percent.

Solution.

Using the EFFECT function in a spreadsheet, we have nominal rate = 0.045 and npery = 12, so we enter

which gives 0.0459 or 4.59%.

Therefore, the APY for an account that pays 4.5% with monthly compounding is 4.59%.

Notes:

If you set the cell format to percentage, the spreadsheet will display 4.59% directly as the result of the formula without having to multiply by 100.

If the spreadsheet shows the result as 0.05, you can click on the "Increase Decimal" button in the toolbar to show more decimal places and see the result as 0.0459 or 4.59%.

Future Value and Present Value.

Future Value:

=FV(rate,nper,pmt,[pv],[type])

Present Value:

=PV(rate,nper,pmt,[fv],[type])

rate is the stated interest rate (APR) and is entered as a decimal.

npery is the number of compounding periods per year.

pmt is the payment amount. If there are no payments, enter 0.

pv is the present value or initial amount. This is entered as a negative number when using the future value function.

fv is the future value or desired amount in the future. This is entered as a positive number when using the present value function.

Variables in square brackets are optional inputs. If you do not have a value for an optional input, you can just omit it when entering the formula in the spreadsheet. If you have a value, enter it but do not type the square brackets.

Example 3.4.15.

Suppose you deposit $3000 in a CD (certificate of deposit) account paying 6% APR, compounded monthly. How much will you have in the account after 20 years?

Solution.

Using the FV function in a spreadsheet, we have rate = 0.06/12, nper = 20*12, pmt = 0, and pv = -3000, so we enter

=FV(0.06/12,20*12,0,-3000)

which gives $10,854.57.

Therefore, you will have $10,854.57 in the account after 20 years.

Example 3.4.16.

You know that you will need $40,000 for your child’s education in 18 years. If your account earns 4% APR compounded quarterly, use a spreadsheet to find how much would you need to deposit now to reach your goal.

Solution.

Using the PV function in a spreadsheet, we have rate = 0.04/4, nper = 18*4, pmt = 0, and fv = 40000, so we enter

which gives $19,258.63.

Therefore, you would need to deposit $19,258.63 now to reach your goal.

Exercises 3.4.6 Exercises

1.

A friend lends you $200 for a week, which you agree to repay with 5% one-time interest. How much will you have to repay?

2.

You loan your friend $100. They agree to pay an annual interest rate of 3%, simple interest. Six months later they repay that loan.

How much did they pay you?

How much was interest?

3.

Consider a simple interest loan of $200 with an annual interest rate of 6%. If that loan is paid off 1 year and 3 months later, how much was repaid?

4.

You deposit $1,000 in an account that earns simple interest. The annual interest rate is 2.5%.

How much interest will you earn in 5 years?

How much will you have in the account in 5 years?

5.

Consider an investment of $20000 with an annual interest rate of 5%.

If that investment is earning simple interest, how much will the investment be worth in 10 years?

If that investment is getting annually compounding interest, how much will the investment be worth in 10 years?

6.

Nico invests $4,500 into an account that has an annual interest rate of 8.5%. The interest is compounding monthly. Twenty years later what is the account balance?

7.

How much will $1,000 deposited in an account earning 7% APR compounded weekly be worth in 20 years?

8.

Suppose you obtain a $3,000 Certificate of Deposit (CD) with a 3% APR, paid quarterly, with maturity in 5 years.

What is the future value of the CD in 5 years?

How much interest will you earn?

What percent of the balance is interest?

9.

You deposit $300 in an account earning 5% APR compounded annually. How much will you have in the account in 10 years?

How much will you have in the account in 10 years?

How much interest will you earn?

What percent of the balance is interest?

10.

You deposit $2,000 in an account earning 3% APR compounded monthly.

How much will you have in the account in 20 years?

How much interest will you earn?

What percent of the balance is interest?

What percent of the balance is the principal?

11.

You deposit $10,000 in an account earning 4% APR compounded weekly.

How much will you have in the account in 25 years?

How much interest will you earn?

What percent of the balance is interest?

What percent of the balance is the principal?

12.

How much would you need to deposit in an account now in order to have $6,000 in the account in 8 years? Assume the account earns 6% APR compounded monthly.

13.

How much would you need to deposit in an account now in order to have $20,000 in the account in 4 years? Assume the account earns 5% APR compounded quarterly.

14.

Breylan invests $1,200 in an account that earns 4.6% APR compounded quarterly and Angad invests the same amount in an account that earns 4.55% APR compounded weekly.

What will their balances be after 15 years?

What will their balances be after 30 years?

What is the effective rate for each account?

15.

Bill invests $6,700 in a savings account that compounds interest monthly at 3.75% APR. Ted invests $6,500 in a savings account that compound interest annually at 3.8% APR.

Find the effective rate for each account.

Who will have the higher accumulated balance after 5 years?

16.

Bassel is comparing two accounts where one pays 3.45% APR quarterly and the second pays 3.4% APR daily.

What is the effect rate for each?

If he has $5,000 to deposit how much will the balance be in 10 years?

17.

You deposit $2,500 into an account earning 4% APR compounded continuously.

How much will you have in the account in 10 years?

How much total interest will you earn?

What percent of the balance is interest?

18.

You deposit $1,000 into an account earning 5.75% APR compounded continuously.

How much will you have in the account in 15 years?

How much total interest will you earn?

What percent of the balance is interest?

19.

You deposit $5,000 in an account earning 4.5% APR compounded continuously.

How much will you have in the account in 5 years?

How much total interest will you earn?

What percent of the balance is interest?

20.

You deposit $10,000 in an account that earns 5.5% APR compounded continuously and your friend deposits $10,000 in an account that earns 5.5% APR compounded annually.

How much more will you have in the account in 10 years?

How much more interest did you earn in the 10 years?